Make Your Business With Us

From anywhere in the world, our complete platform simplifies the Bangladesh company registration, allowing you to establish your business. JK Associates" company formation for non-Bangladesh residents. Easily start a Bangladesh business, online.

Your Trusted Advisors in Business Success.

"JK Associates"is top-ranked Corporate Consultancy and Law firm in Bangladesh with the international presence provides specialized services in Intellectual Property Rights, Corporate Affairs, Foreign Trade and Investment, Taxation, and Litigation.

850+

Global Clients

10+

Specialists

8+

Year of experience

The One-Stop Solution For Entrepreneurs

On-the-ground experts

Unlike competitors, we have a fully-fledged tax team based in Bangladesh. Our experts are directly involved in a situation or are at the place of your interest. Get answers through the app’s live chat, via email, or phone for easy access to advice and in-person consultation.

Get service remotely

Start a company and open an Aspire business account from anywhere in the world.We assist you online and help you with local compliance.

Tax right from day one

We give you guidance on the best business structure, set up your accounting, and inform you on tax reliefs available to your business so that you're set up to pay tax efficiently from the get-go.

Long-term Compliance support

Regulatory compliance support helps organizations maintain integrity, protect their reputation, and avoid penalties. It includes ongoing attention to regulatory changes, employee training, policy updates, and risk management, beyond initial setup and annual audits.

VAT Calculator

Where Global Entrepreneurs Thrive

We make launching your Bangladesh business easy, fast, and effective

Get Started

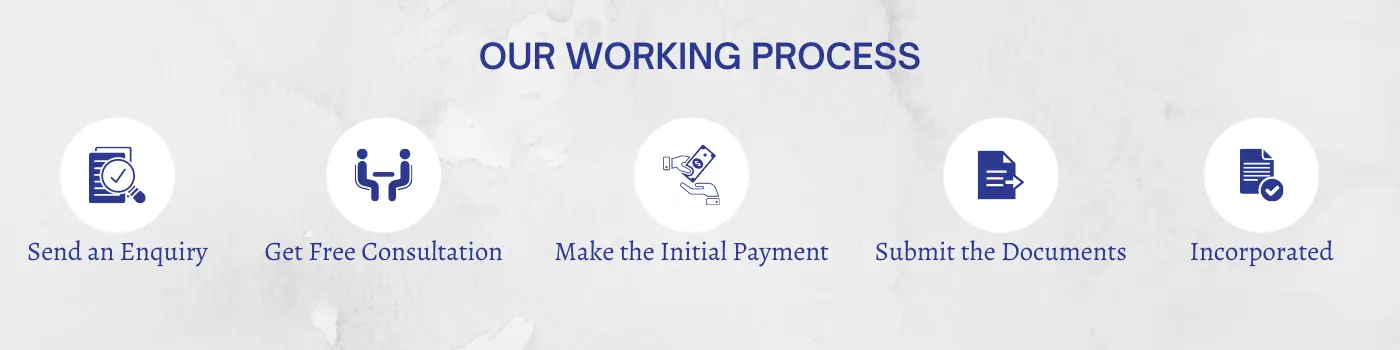

How to open Company in Bangladesh

Step-1

Proposed Name Search & Application

Request free company name search. We can check the eligibility of the name, and make suggestions if necessary.

Step-2

Prepare Company Details

- Approval proposed company name.

- To draft the memorandum of association (MoA) and articles of association (AoA).

- RJSC Register or login and online fillup in the company names and director/shareholder(s) details.

- Fill in the company address with share capital, other details (if any).

- If, the foreign equity company in Bangladesh. Open a bank account for the proposed company and transfer equity capital or transfer inward remittance from abroad and request for encasement certificate for foreign equity company registration to the bank.

Step-3

Payment for your company

- Register or login into the RJSC portal for check and final submission.

- Before the final submission, attach the zip file and encasement certificate for foreign company registration.

- To generate submission ID and acknowledgement slip.

- To communicate with concerned authority.

Step-4

Send the company kit to your address

- You will receive soft copies of necessary documents including: Certificate of Incorporation, Memorandum and Articles of Association, Form XII.

- You can bring the documents in the company kit to open a corporate bank account or we can help you with our long experience of Banking support service.

- Before the bank account opening you required the company tax certificate, trade license and rental deed, company seal stamp and board resolution on the official pad. Then your new company in a jurisdiction is ready to do business.

Frequently Asked Questions

Trademark Registration Process. Step 1: Searching for Trademark Registration . Step2: Power of Power of Attorney Step 3: Filling an Application for Trademark Registration, Next Up to Final Registration.

Customer Experiences With Us

2 months ago

I recently had the pleasure of working with JK Associates to complete my tax return and I was impressed with their service. From start to finish, their team demonstrated exceptional professionalism, efficiency, and expertise.

1 year ago

My experience with JK Associates was a very positive one. Their service was very professional and swift. Highly recommend JK Associates, especially for foreign nationals working in Bangladesh who look for trusted tax consultants.

8 months ago

Your exceptional work not only demonstrated a deep understanding of our needs but also showcased a level of commitment and passion that truly touched our hearts. Your contributions have been invaluable, and we're grateful for the positive impact you've had on our endeavors.